The Philadelphia Office of Budget and Program Evaluation works under the Office of the Director of Finance, assisting it with developing operating and capital budgets for the city. In its executive function, the office works to monitor legislation developed governing appropriation bills and performs a supervisory role in the approval of city spending and project requests where relevant. On an annual basis, it manages the budget allocation process by taking the requests of city departments into consideration and tabulates a budget for the year ahead based on incremental modifications to prior year budgets.

The office also performs a function of information dissemination. On a timely basis, the office generates periodic projections of indices indicative of growth outlook and the economic climate in the city. These include the Comprehensive Annual Financial Report,

Supplemental Report of Revenues and Obligations, Summary of the Operating Budget and Five Year Financial and Strategic Plan, which serve to generate transparency and fiscal accountability in regard to the work of the city. The mission of the office, therefore, focuses on integrating the executive and informational aspects of its work to offer strategic recommendations on how Philadelphia should identify its main developmental priorities, allocate its resources as a city to attain these objectives and coordinate effectively with subsidiary agencies to execute these changes.

A core tenet defining the professional history of the Office of Budget and Program Evaluation has been its goal to align the budget with the main goals of the Mayor’s office. For instance, the latest five-year plan detailed additional funding toward supporting extended hours for the Free Library to expand hours in neighborhood branches, new investments in the KEYSPOTS program following the termination of federal funding sources and support for the Community College of Philadelphia. The innovation of budget reform aimed to better inform resource allocation and decision-making processes in order to enhance the city’s ability to achieve strategic objectives and outcomes.

Problem Formulation

For previous budgets, the city had always utilized a conventional incremental budgeting process to determine budget allocations. Each year, the previous year’s budget for each department was obtained and utilized as the benchmark. The office would proceed with projecting revenues in advance of the budgeting process, develop an overall figure for the total amount available for distribution and

determine upcoming allocations using historical appropriations as the basis. In a flat or declining budgetary climate, departments had to possess a sufficiently compelling rationale in order to obtain an increase in budget allocation. This caused problems given the current structure and expectations of urban governance. With a focus on the levels of inputs rather than outcomes, this method does not provide a manner in which the value added by different services could be compared uniformly.

This focus on resource needs rather than outcomes made it difficult for policy makers to make informed decisions regarding the scale of providing government services. In order to accurately quantify the extent of a problem and determine the level of resources necessary to address it, policy makers needed to know where the city was in terms of providing service levels, the unit costs associated with delivering those services and the marginal benefit that further allocations could bring to the city. Program-based budgeting, which has been implemented successfully in other cities, offers a more responsive and accountable form of budgeting that emphasizes outcomes instead of inputs when compared with incremental budgeting. However, this entails the creation of a system dependent upon clear definitions and measurement of performance metrics within and across departments. The city faces a situation of limited data, which presents an obstacle to its progress toward program-based budgeting.

Breakthrough Innovations In Government

For an organization that has traditionally relied heavily on an incremental approach to budgeting based on historical allocations, opting for an approach predicated on accurate and timely cost and performance data can certainly be characterized as a radical transition. Breakthrough innovation, as it is commonly known, has recently begun to permeate governments, despite the glaring absence of the profit motive driving such phenomena in the private sector. What then assists these innovations in their creation and survival? Clayton Christensen, Kim B. Clark Professor of Business Administration at the Harvard Business School, led a research group to develop a framework for understanding such innovations in government, drawing from a multiplicity of sources including hundreds of government initiatives, government municipalities, public-sector innovators and expert panels. These have crystallized into an enabling framework:

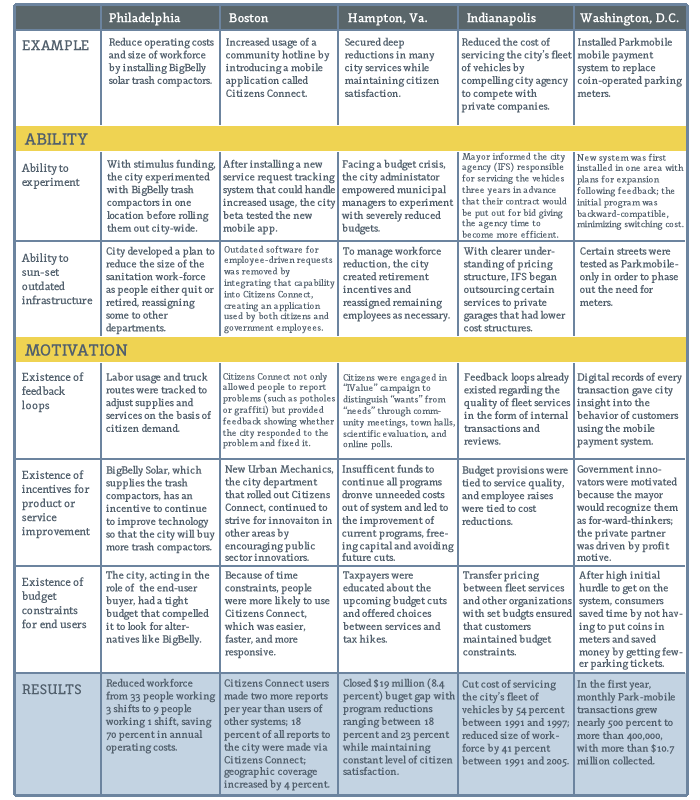

Ability to Experiment – Under Mayor Nutter’s tenure, the Office of Budget and Program Evaluation had specifically been charged with the objective of ensuring alignment between the five strategic goals of his administration and the current fiscal priorities. These necessitate the maintenance of clear outcomes and performance metrics to accompany each of these goals. The city has also emerged recently from the debilitating financial crisis and economic recession, providing it with slightly more budgetary flexibility and room to explore alternative methods of managing expenditures instead of implementing across-the-board cuts. Implementing performance management for the budget would facilitate more effective resource deployment in the long run, which is possible now since the city does not face immediate pressure to cut departmental budgets. Recently, the City Council passed an ordinance, approved by the voters and supported by the Nutter Administration, that requires the city to move towards program-based budgeting.

This has provided the office with a change mandate and considerable leeway to experiment with and define a new budgeting approach.

Ability to Sunset Outdated Infrastructure – The current methods of recording budgetary information rely on the maintenance of spreadsheets existing entirely within Microsoft Excel. This makes transferring and consolidating information across departments a manual and time-consuming task. Moreover, no central data system exists to track departmental performance and program costs. The budget office is in the process of procuring budget formulation systems that will allow departments to submit their budgets and performance data online. This presents an improvement from the original system because it will automatically consolidate and manipulate data, eliminate substantial amounts of manual work and allow the budget office to track and connect performance data with cost information. This is a critical piece that is enabling the budget office to take on this budget reform effort.

Existence of Feedback Loops – The existence of vocal feedback channels to the office has enabled them to tune in to the concerns of stakeholders directly affected by the system. These include the beneficiaries of budget allocations and taxpayers who contribute to the city’s spending power, including residents, small businesses and other dependents who have been reliant on city services.

Much of the feedback has emerged from the executives utilizing the budgets on a first-hand basis. Foremost, the City Council comes to mind, having pushed for the program-based budgeting transition. The council plays an active role in reviewing the mayor’s proposed budget, weighing in on modifications and accepting the final budget as well as providing oversight of the administration and its performance.

Recently, the City Council passed an ordinance requiring the administration to move toward program-based budgeting. Its desire to see what the precise tradeoffs are between competing allocations for the city’s financial resources has translated into the city’s being compelled to move toward program-based budgeting.

Staff members within the office who have had similar experiences working in other cities have also compared the city’s current technological system with more advanced ones that have been implemented across the country. Their external perspectives on quick wins available to the system, such as the creation of a single central repository for all performance information, have helped galvanize the push toward this new innovation.

Existence of Incentives for Product or Service Improvement – Implementing program-based budgeting would compel participating departments to reduce waste and maximize outputs, thus freeing up excess capacity that could be funneled toward discretionary spending that supports mayoral objectives.

Theory of Change

Underpinning the entire innovation is its theory of change. The individuals spearheading the innovation, Rebecca Rhynhart and Fiona Greig, firmly believe that moving to a program-based budget will compel city departments to identify core programs and services that the department is responsible for. This will assist them in prioritizing the goals that each department has sought to achieve and in better calibrating financial inputs toward achieving strategic outcomes.

Utilizing the Philadelphia streets department as an illustration, performance metrics could be framed in terms of the tons of solid waste or tons of recycling collected. The information would help inform the budget in regard to how monetary values translate to program outputs, answering difficult questions such as the cost to the city per ton of solid waste collected. Since many of the city’s priorities goals and goals are framed in terms of tangible non-monetary outputs, translating a financial budget into similar terms will help policy makers better understand allocation requirements.

Apart from achieving a distribution of resources that enhances the attainment of priorities, this change also facilitates greater scrutiny and evaluation of each department and its programs. How effectively do they manage the resources they are allotted? Are their outputs directed at accomplishing outcomes and objectives prioritized by the mayor? This forms the foundation from which incentives can be structured to reward departments for their performance and create greater accountability.

Personnel

The office brings a talented team to bear on this project, with complementary skill sets fully capable of overseeing the change in methodologies. Rebecca Rhynhart, director, has had extensive experience in industry and public finance, having worked at Bear Stearns. Her experiences interacting with stakeholders at the budget office and familiarity with the various processes that go into the development of the budget have positioned her well to take charge of discussing the idea with partnering departments and getting them to buy into the idea. Fiona Greig, who received her PhD in public policy, last worked at McKinsey, overseeing numerous large-scale change management projects, and she is well placed to oversee the execution process. Her background lends itself well to the task of conceptualizing and refining the innovation methodology that she has assumed on this team. The team has worked in collaboration with the PhillyStat team, the city’s other primary performance management function, and prepared performance reports such as the quarterly city managers report and the Five Year Financial and Strategic Plan, bolstering their expertise in the domain.

Comparable Innovations

The idea of program-based budgeting is nothing new. While Philadelphia is not an early adopter of the innovation, since other cities have already implemented innovations of a similar nature, a scan of the largest cities indicates that most of them have not implemented a similar system due to its extensive data requirements. Therefore, San Jose’s Management Performance Program is

uncommon, and an example that the current innovation seeks to be modeled after. The extent of their innovation can be modeled along three distinct aspects.

Budget Call: City service areas focus on developing service delivery and investment strategies for the upcoming budget process. In addition, the city service areas incorporate strategic planning and City Council direction into results-driven spending plans.

Budget Cycle: The budget cycle is developed on an annual basis.

Performance Metrics Collated: For each measured service, quality, cost, cycle time and customer satisfaction were evaluated. In addition, output and outcome levels were tracked in terms of their actual, forecasted, targeted and estimated values.

The situation in Philadelphia remains marginally different from that in San Jose, given that Philadelphia already has an agency dedicated to defining, measuring and tracking the goals that the mayor has established.

Impact Analysis

The budgeting innovation is likely to improve the city’s ability to allocate resources more effectively on a tactical basis within strategic priorities and eliminate waste. For instance, certain departments within the city could potentially fulfill overlapping functions. The innovation’s implementation provides a means of deciding between two allocation alternatives.

A secondary pecuniary benefit is that program-based budgeting enables the city to prioritize outcomes it wants to achieve given budget constraints. It allows the mayor to decide how he or she would like to invest the incremental revenue the city collects as the economy improves. Does he or she want to place 100 more residents in jobs, provide free Internet access to 2,000 more residents, plant 1,000 more trees cut in half the city’s 311 hotline call wait time or some combination of the above?

Finally, program-based budgeting will create greater transparency about the unit costs of central services, such as the cost of managing a square foot of the city’s building space. This information is extremely useful since it would enable departments to understand and account for the total cost of service delivery rather than just the direct costs. The city could thus gain insight into the degree to which departments and programs use central services (such as office space) more or less efficiently and increase accountability and incentives for departments to use these services more efficiently. Therefore, the overall productivity of the service delivery process could improve. These efficiency gains from the innovation are therefore far from marginal.

Conclusion

The long-term ramifications of this budgeting innovation are undeniable. Distinct from implementing beneficial change from a top-down level, the innovation has tremendous potential to initiate bottom-up change. The eventual creation of a holistic performance-based management system will enable large-scale publicizing of performance metrics in line with current budgeting figures, similar to what has been achieved on statewide levels in places such as Oregon. The widespread availability of performance data governing the city’s service delivery standards will allow the office to involve a large number of citizens in the decision-making process by providing them with enough information so that they can form opinions in determining what outcomes would benefit them most significantly or what the trade-offs are in deciding between competing areas of funding. The provision of more detailed information would mark a step ahead for democratic participation, since information empowers citizens and incentivizes them to act on issues.

The changes will also have a cascading effect on the subsidiary departments dependent on the city for funding. It will compel them to undergo a thorough inventory of capabilities and skill sets, evaluating whether these are suitable for the outcomes they have been tasked to achieve. Aside from this streamlining of organizational structures, the greater transparency accruing to the central

decision-making bodies will compel departments to be more careful in monitoring their expenditures and minimizing waste.

The sustainability of the innovation in the long term is also a continual concern that plays into this analysis. While the implementation of a central database to coordinate all incoming data feeds is an isolated occurrence, converting all of the city’s departments to a program-based budgeting system will require continued advocacy to generate extensive buy-in from a larger group of shareholders. Therefore, it is likely that members of the office will be required to remain on the project.

Acknowledgement

I would like to thank Fiona Greig for her sharp insights and valuable suggestions on improving the structure and accuracy of this piece, as well Nick Torres and Tine Hansen-Turton at the Journal for providing me with the frameworks and contacts I needed to put this piece together.

Bio

Samuel Lim has had several years of research experience relating to collaborative governance structures and idea diffusion within a policy context. He is currently pursuing a PhD in systems engineering and recently completed a master’s in public administration at the Fels Institute of Government at the University of Pennsylvania.

References

Sahni, N. R. (2013). Unleashing breakthrough innovation in government.

Stanford

Philadelphia Social Innovations Journal Article

Samuel Lim

Social Innovation Review.

Retrieved from

http://www.ssireview.org/articles/entry/unleashing_breakthrough_innovation_in_government